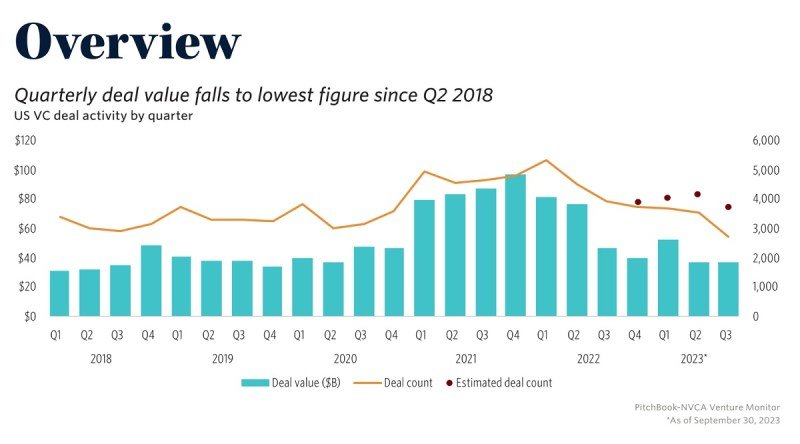

Enterprise capital funding within the U.S. fell to its lowest degree in six years by way of enterprise deal worth and the bottom degree in deal rely in three years through the third quarter.

The Enterprise Monitor report from the Nationwide Enterprise Capital Affiliation confirmed U.S. VC exercise fell to its lowest deal worth degree since Q2 2018.

“The final 18 months have seen a degree of tumult within the financial system that will have been unimaginable only a few years earlier, however amid stormy seas, VC stays nicely positioned to journey the waves,” the report mentioned.

Whereas generative AI exploded this 12 months, geopolitics — not even counting the newest conflict in Israel and Gaza — inhibited the keenness, with the inventory market displaying that buyers are cautious.

Deal counts are on monitor to have the bottom 12 months since earlier than the pandemic in 2019. Total, the market stays beneath appreciable stress, the report mentioned. Extra corporations are taking bridge, continuation, or down rounds; inside rounds are at multiyear highs; and there are fewer rounds with a brand new lead investor acquiring a board seat than at any time in at the least a decade. Traders and founders alike are optimizing for stability and money circulate to fulfill the challenges of the present market.

Nonetheless, the ecosystem stays nicely capitalized, and extra sources of liquidity from federal applications just like the Inflation Discount Act and the CHIPS and Science Act have gotten out there.

In the meantime, the inventory market’s low multiples in value/gross sales ratios for public corporations are inflicting IPOs to dry up. Present estimates place the variety of corporations ready to go public at 75, and whereas exit exercise is predicted to be modest within the close to future, the upcoming listings of family names like Stripe, Chime, and Reddit might portend a extra strong liquidity surroundings.

And pre-seed and seed deal counts within the U.S. have hit a 12-quarter low, or the bottom since 2020. On the entrance finish of the market, the relative share of pre-seed to early-stage offers dropped persistently over the

previous 12 months.

Compared, late-stage and venture-growth offers have been on a comparatively flat pattern over the previous

a number of quarters. There has additionally been a marked lower in megadeals over the previous 12 months, with offers over $100 million making up 48.5% of deal worth in Q3, a far cry from their 60.0% of deal worth in This autumn 2021.

Seed deal counts themselves are on monitor to fall beneath pre-pandemic numbers.

Offers are nonetheless concentrated in regional hubs throughout the U.S.

Feminine founders are discovering the market to be notably tough.

Q3 exits noticed an uptick primarily due to the Instacart and Klaviyo IPOs. Exits through mergers are carrying extra regulatory dangers. In July, the Federal Commerce Fee (FTC) and Division of Justice (DOJ) laid out new pointers for approving mergers. The NVCA mentioned it has plenty of issues in regards to the new FTC pointers, which it mentioned considerably elevate the chance of small firm acquisitions being blocked for theoretical causes which have little underpinning in actuality and misrepresent nascent companies that fall nicely wanting having monopoly energy as being “dominant.”

Lastly, fundraising for brand spanking new VC funds hit a nine-year low. In 2022, fundraising was concentrated within the arms of the biggest funds, with practically half of all capital dedicated going to funds over $1 billion. The relative share of dedicated capital to funds valued between $100 million and $1 billion elevated sharply over the 12 months, making up practically two-thirds of funds raised in 2023 to this point. Regardless of the stronger relative efficiency of mid-cap funds, 2023 has been a tough 12 months for rising managers attempting to lift first funds, with practically three out of each 4 {dollars} raised in 2023 going to a longtime supervisor and first-time funds pacing towards their lowest rely in roughly a decade.

In different data, software program offers are at a multiyear low, whereas life sciences funding, whereas down, is on the highest relative degree since 2020.